From SaaS to AI: The Future of Intelligent Enterprise

The SaaS is dead narrative is getting ahead of itself – it assumes that foundation models will consolidate the entire enterprise tech stack, AI will eat SaaS, and IT and BPO services are dead. We believe this is far from the truth.

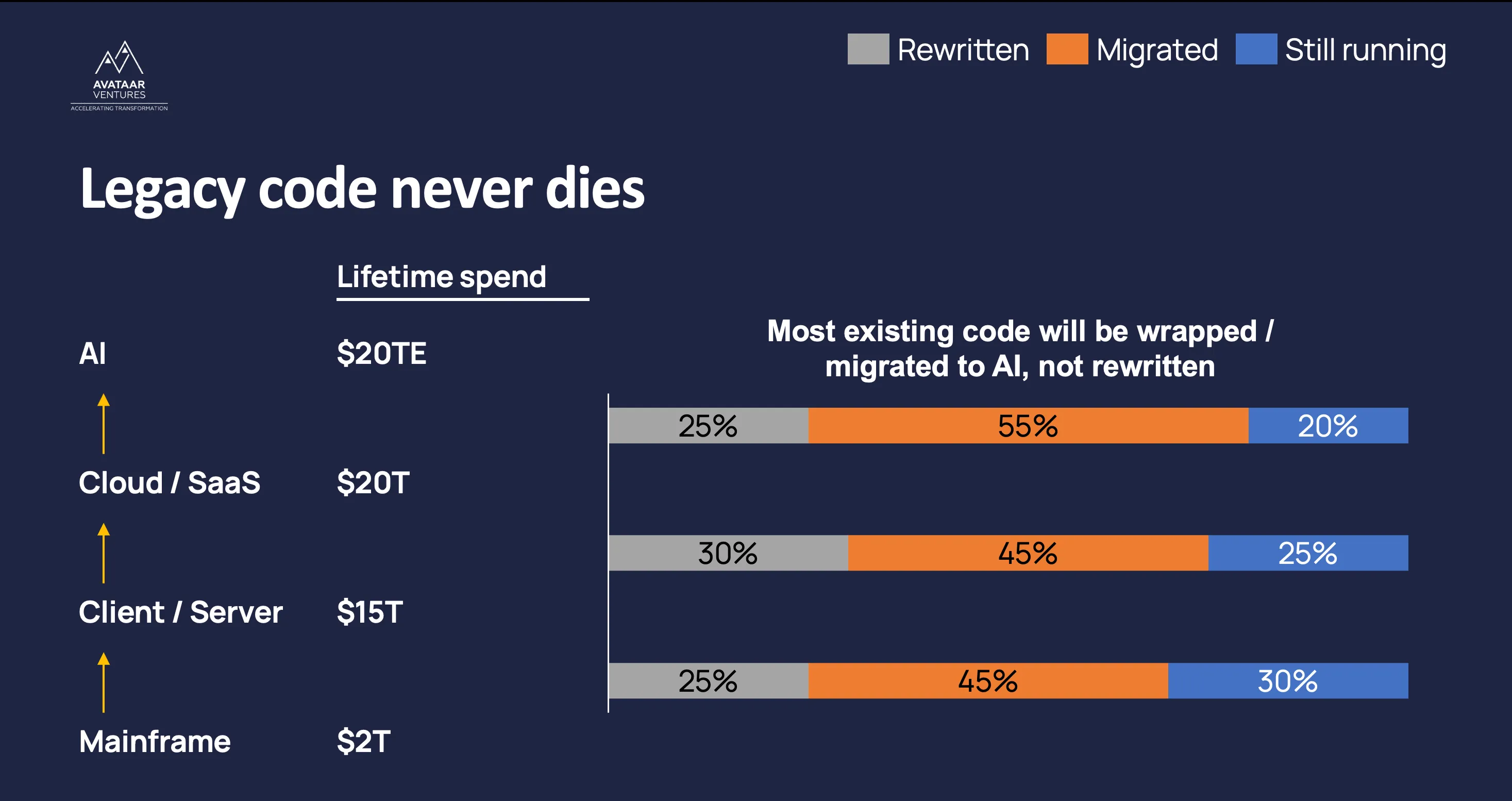

Our view: History shows that legacy code never dies, it gets wrapped. SaaS will evolve into AI and become more valuable.

Let’s examine the past tech evolutions and project the future of SaaS.

Mainframes, launched in 1960s, are stillthe dominant technology running our banks and airlines and contribute a largepart of revenue for IBM.

Client/server tells the same story - Oracle, SAP, and Microsoft - the nativeplayers of that era - are today's enterprise behemoths, still generating most of their revenue from architectures that predate the cloud. Large parts of the code bases of these technologies have been wrapped and migrated to the next evolution, not killed.

We believe SaaS to AI evolution will follow the same pattern as past. It’s too valuable, entrenched, and expensive to kill. AI will abstractSaaS, not displace.

Over the past two decades, enterprises have poured north of $20 trillion into SaaS. That’s not just software spend — that’s institutional memory encoded in workflows, schemas, permissions, and integrations. Enterprises are unlikely to rip that out overnight.

The real asset of Salesforce or SAP is the structured, labeled, workflow-rich data underneath. Decades of business logic, edge cases, approvals, and exceptions.

AI doesn’t replace that; it feeds on it. Without SaaS, most enterprise AI would be starved of context.

There’s also a harder truth: organizations themselves are the bottleneck. SaaS is deeply embedded in how teams collaborate — who owns what, how decisions get made, how accountability flows. This is exactly why enterprise AI adoption is still uneven. It’s not a technology problem; it’s a change management problem.

And then there’s compliance—the silent anchor. Billions are spent every year on identity, permissions, audit trails, contracts, and data governance across sprawling SaaS stacks. AI-first tools don’t magically inherit that trust layer. Rebuilding it from scratch is not just difficult, it’s existentially risky for large enterprises.

So what is the future of SaaS?

SaaS becomes the substrate for AI. Expect 50–60% of SaaS code to be “wrapped”—not rewritten. The UI will shift from dashboards to conversations. The logic will move from rigid workflows to probabilistic reasoning. But underneath, the same systems of record will persist, quietly doing what they’ve always done: storing truth and serving the indispensable business context. Winners will evolve SaaS, not try to replace it.

Our 4 predictions on evolution of SaaS to AI

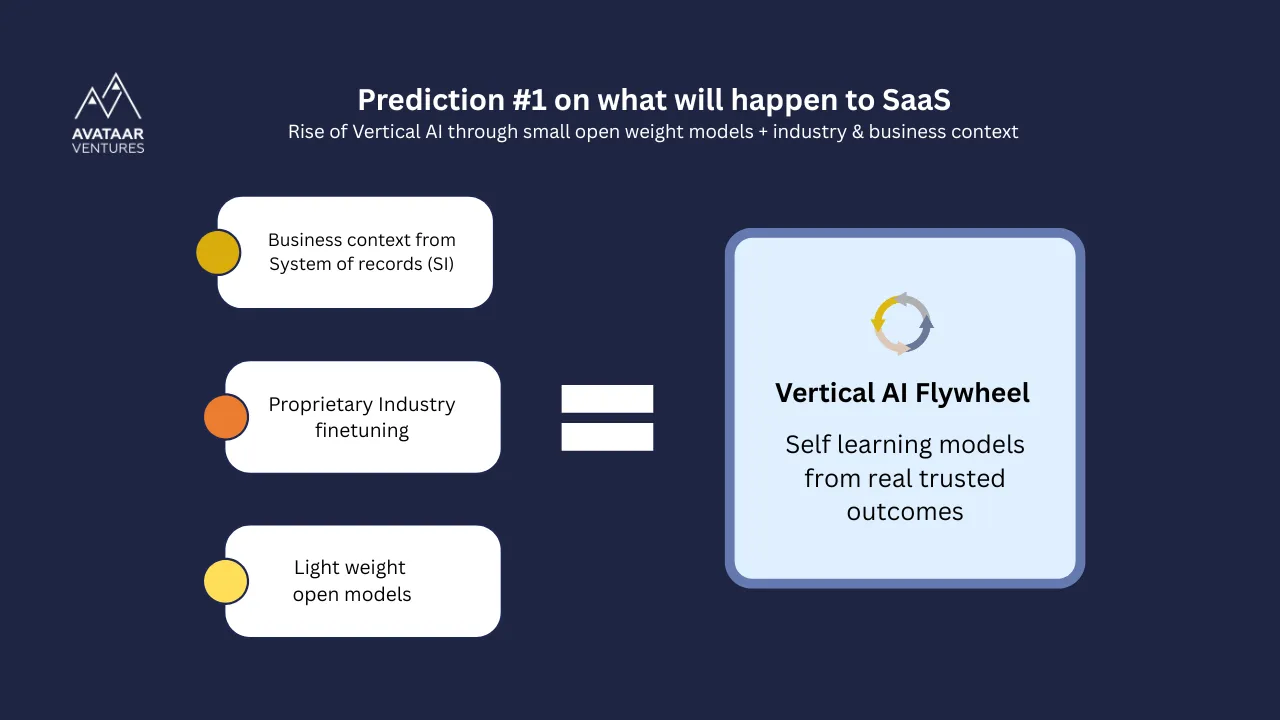

Prediction # 1: Rise of Vertical AI through small open weight models + industry & business context

Pundits advocate a utopian view of all-encompassing large foundational models. However, we believe their limitation is fluency without context.

Value for enterprises comes from deep understanding of workflows, edge cases, and domain nuance. Foundation models with their generic intelligence will dominate horizontal productivity and prosumer use cases, but fall short for vertical Enterprise needs in predictability, security and cost.

We believe Vertical AI stack will consist of light open weight models (e.g., Qwen, Mistral, Llama) trained on proprietary industry data and deeply integrated with system of record that provides user’s specific business context. This will be topped with a proprietary AI flywheel that uses actual operational trusted results to continuously sharpen the model on real-world performance rather than internet text.

Andrej Karpathy calls this "model speciation,” i.e., smaller models that outperform general ones in specific niches, not through brute scale, but through cognitive fit. Intercom has proven it – they claim their Apex model trained on billions of proprietary customer service interactions outperforms other foundational models and is faster and cheaper.

Generic large foundational models will be limited to horizontal and prosumer use cases. Enterprise Vertical AI stack will consist of light open weight models + industry data + SaaS-fed business context.

Prediction #2: The migration will create new categories — and new giants

The client/server-to-cloud migration consumed roughly $1.5 trillion across vendor R&D, customer IT spend, and System Integrator/consulting fees. And it is still only 25–40% complete.

That migration created entirely new categories: middleware to make data available in distributed environments (Tibco, Mulesoft, Apigee), databases and observability tools (Snowflake, Datadog, Dynatrace, New Relic), and DevOpstools for CI/CD (GitHub, HashiCorp).

The SaaS-to-AI migration will do the same.

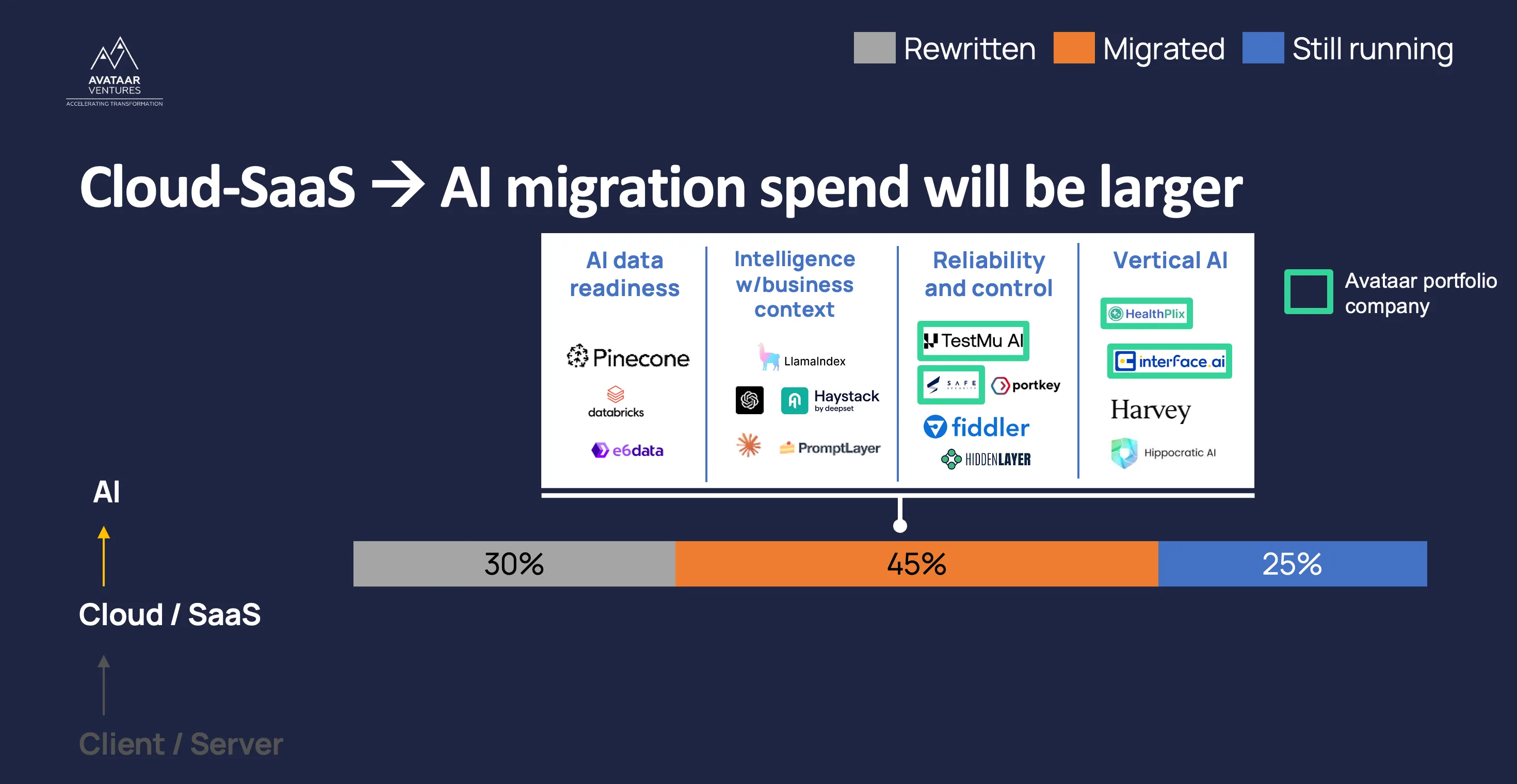

We are already seeing new categories emerge – for example

- AI data readiness including vector databases, unstructured data processing, and real-time fast analytics.

- Intelligence with business context across RAG, reinforcement learning, and enterprise-tuned models

- Reliability and control unique to AI — evaluations, governance, gateways, and security

While AI-native tools will accelerate parts of this shift, the sheer volume of migration will drive spending to levels comparable to past transitions.

The SaaS-to-AI transition will create entirely new infrastructure categories—and new winners. Incumbents will struggle to adapt.

Prediction #3: System Integrators will get a Second Act - again!

System Integrators (SIs) win in transition moments. Accenture, Infosys, Wipro, and TCS built empires helping enterprises adopt cloud — from data modernization to building middleware (enterprise bus) to implementing and managing SaaS systems.

AI is no different. It is complex and cuts across sensitive change management topics: systems, data, security, workflows, people, and operating models. Professional support is not optional. However, AI service delivery will require a new playbook and different set of unit economics – a crack team of domain experts powered with repeatable proprietary accelerators and industry context, contracted for fixed fee with some skin in the game (vs. the traditional Time & Material model) and delivering accelerated implementations with rich margins.

We are already seeing this play out. Palantir and OpenAI are promoting the concept of Forward Deployed Engineers — essentially specialized services teams mandated to implement AI. Infosys and Anthropic announced a collaboration integrating Claude models (including Claude Code) with Infosys Topaz, aimed at automating complex workflows and driving adoption in regulated industries.

The winning Enterprise AI adoption playbook: Specialized services provider + Vertical AI stack + enterprise change management wrapper.

Prediction #4: The overlooked opportunity ~4,000 stalled SaaS and IT/BPO companies ready for reinvention

Beneath the noise of AI disrupting SaaS lies a quieter, more compelling story – there are roughly 4,000 SaaS and IT /BPO services companies globally that reached meaningful scale of $10M to $100M in ARR but growth has stalled due to rising competition, lack of funding, or missed platform shifts.

These are high quality assets that possess something deeply valuable: entrenched customer bases, years of proprietary workflow data, hard-won domain expertise, and trusted vendor relationships that new entrants would take a decade to replicate. Importantly, many of these companies are now trading at a fraction of their peak valuations—often 3–5x ARR versus the 15–20x highs of 2021.

This creates a compelling wedge for AI-driven reinvention. AI infusion can convert static, rules-based software into intelligent, agentic products: systems that learn from usage patterns and intelligently automate complex workflows. Crucially, this sidesteps the hardest part of building an AI-native company from scratch — the decade-long slog of go-to-market, customer trust, and workflow integration.

The playbook is straightforward: acquire at discounted multiples, infuse AI into the core product, expand TAM through new AI-native use cases, and re-rate at AI-era multiples as the business compounds. And it favors patient, operationally hands-on investors who can combine M&A discipline with product and AI execution.

Roll-up playbook: acquire at discounted multiples, infuse AI, expand TAM through new AI-native use cases, scale organically & inorganically, and re-rate at AI-era multiples. This is not a venture playbook.It’s an operating VC playbook—and only a handful of funds are built to execute it.

This is what we built Avataar to do.

We are an operating VC fund with a dedicated operating team that specializes in business growth and AI infusion — domain experts, AI specialists, and a network of global GTM advisors working alongside founders inside the company, not from the sidelines.

We have run this playbook before. RateGain, Capillary Technologies, and Amagi — three companies that grew organically and inorganically under our partnership and listed on Indian public markets. Each started as a scaled but stalled business. Each needed operational intervention to break through.

The AI transition does not change this playbook. It accelerates the timeline and widens the aperture.

.webp)

.webp)

.webp)

.webp)

_page-0001%20(1).webp)

.webp)