SaaS AI Displacement Framework: Early Warning Signs, Transformation Levers, and What We Are Seeing in the Portfolio - PART 2

In Part 1, I laid out the 2x2 framework — two axes, eight scoring dimensions, four quadrants — and asked you to be honest about where you sit. If you have not read it yet, start there. You can also directly get your score on this tool we built.

Everything below assumes you know which quadrant you are in.

It’s worth calling out that of one of the 100+ founders that evaluated themselves on the framework, there were few repeat patterns we observed:

- Most founders place themselves in the safe quadrant. Several of them landed in Proprietary Data + Workflows, the lowest-risk position. Self-assessment tends to be generous about one's own moat.

- Revenue scale did not buy safety. The high-risk scores were not confined to pre-revenue founders. One sat in the $25M-$50M ARR band. Early as this is, it raises the question the framework keeps returning to: defensibility is a function of where you sit in the matrix, not how much ARR you have reached.

- Overall, majority of founders fared well on Workflow v/s Data. This speaks to the strength of most SaaS-era founders who have built neat workflows on top of existing systems of record.

This article covers three things:

- How to know if your position is eroding even when the numbers still look fine (early warning indicators)

- What specific moves can help you shift quadrants

- What these transitions look like inside real companies

The numbers can lie to you

The problem with quarterly dashboards is that they are lagging indicators. The early warning signs of AI displacement are subtler, and they are different depending on where you sit.

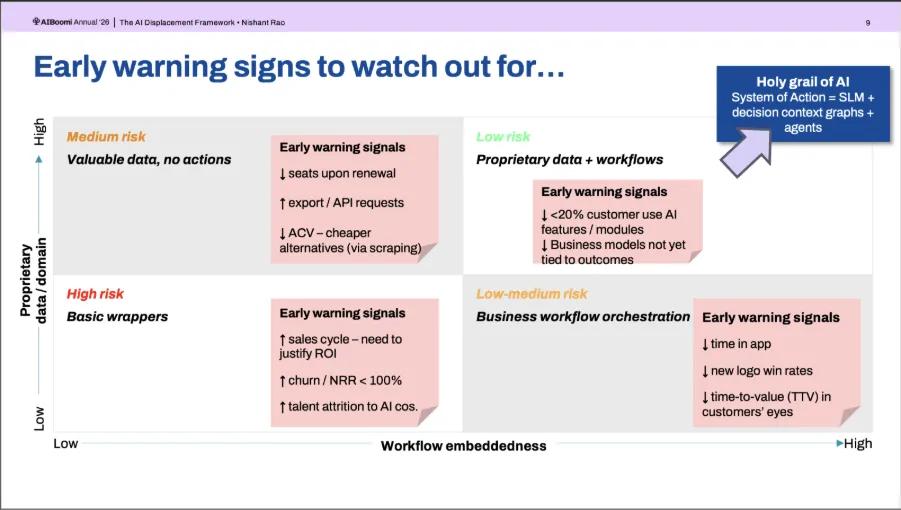

If you are in the top-left — valuable data, no actions — watch out for three signals:

First, seats declining on renewal. It will look like your customer is still there, but they’re just buying fewer licenses. They are likely figuring out how they can get 80% of the value from one seat instead of five (eg. Internal AI initiatives to drive team productivity and/or feed new AI tools using your data)

Second, export and API requests rising. Someone is pulling your data into another system. That is not engagement. That is proactive steps being taken for extraction.

Third, ACV compression. A cheaper AI-native alternative has emerged; often built on scraped versions of data you thought was proprietary.

If you are in the bottom-left — basic wrappers — the signals are louder and the writing is already on the wall. Sales cycles lengthening because buyers now demand ROI justification before signing. Churn accelerating, with NRR sliding below 100%.

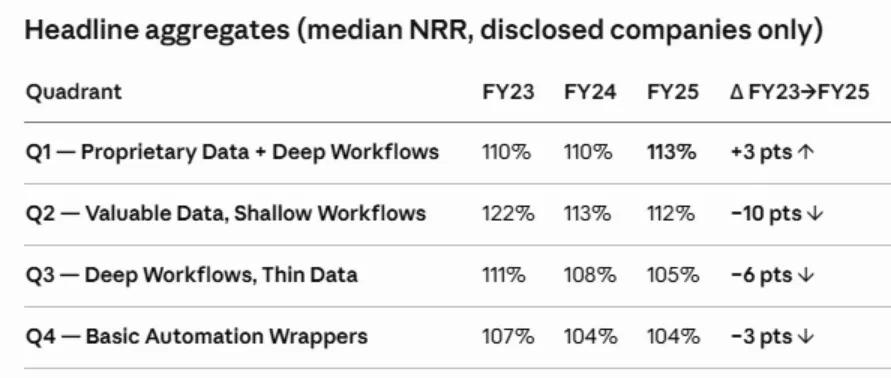

We looked at 70+ US-based public SaaS companies and ran a proprietary analysis on their NRR and here are the trends we found.

Q4 has 6 companies including names like Asana, Weave, Yext trending sub-100 NRR now.

You should also look at if your best engineers are leaving for AI-native companies. That one hurts the most because it compounds the other negative markers.

If you are in the bottom-right — workflow orchestration — the signs are quieter but just as dangerous. New logo win rates are falling since they have newer AI-native solutions to choose from. And while your current customers are (for the time being) locked in, their users may be spending less time in your product because something else is doing part of the job and/or they are just biding time until the renewal. Basically, customers are telling you — or worse-yet telling their peers— that your time-to-value feels slow compared to what AI alternatives promise.

If you are in the top-right — proprietary data and workflows — you are in the safest quadrant, but do NOT confuse position with momentum.

Watch for AI feature adoption. If fewer than 20% of your customers are using the AI modules you have shipped, that is a red flag. It means your AI is a checkbox, not a product.

Also watch whether your business model is tied to outcomes. Both customers & investors now expect deprecation of seat-based pricing. Either you’re creating enough ROI / value (in which case you deserve to claim some of that upside) or you’re perceived as being out of touch so they should start looking for other options whose pricing models are more aligned to the customer’s success.

None of these are death sentences. All of them are signals that your current quadrant is not as stable as your board deck suggests.

The moves that actually work

Knowing where you are is the diagnostic. Moving is the work. And the playbook is different for each quadrant.

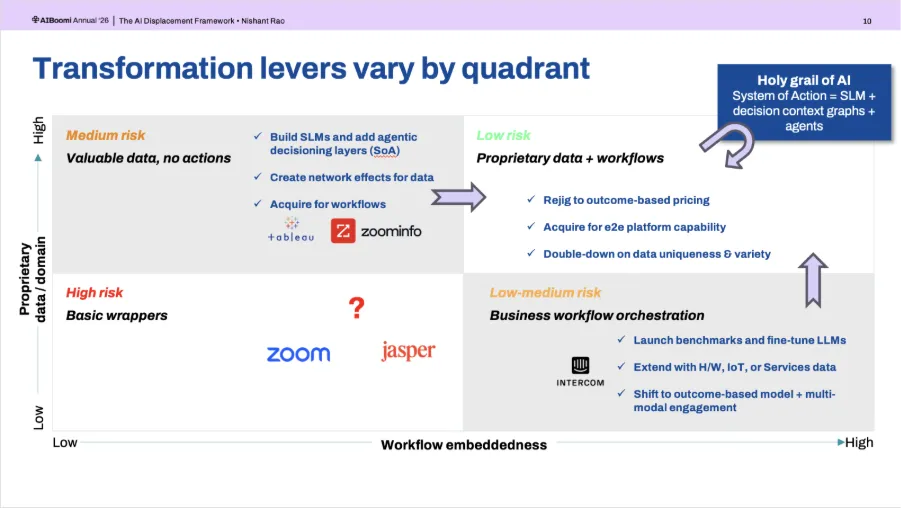

From the top-left (valuable data, no actions) — move right. You have data. You need workflow. You can use three levers:

Build small language models trained on your domain data and add agentic decisioning layers on top to try and move towards becoming more of a System of Record or ideally System of Action. For example: Bloomberg was always known for its strong data but realized that they are exposed to disruption if an SoR starts to pipe in its own data feeds. Hence they built out AIM (a buy-side order & investment management system) and acquired Broadway Technologies (sell-side execution management system). Together, these enabled Bloomberg to go from "terminal you look at before trading" to "platform that executes the trade."

Another way to move right is to acquire a company that already has the workflow embeddedness you lack. This is what Tableau attempted when Salesforce bought it — take proprietary data visualization and embed it into an existing workflow platform. Contrast this with ZoomInfo who tried a version of this with its acquisitions for lead scoring and outbound orchestration. However, their mistake was the strategy to “synchronize with CRMs” vs displacing / owning the CRM thereby capping their own workflow embeddedness potential. Another success criteria worth calling out is the need to ensure the acquired company is integrated deeply vs just “bolted on”.

Finally, you should look to create network effects so that each new customer makes the data more valuable for every other customer.

From the top-right (proprietary data and workflows) — move up. You are in the strongest position. Do not waste it by standing still. Use the below three levers:

Shift to outcome-based pricing so your revenue scales with the value your AI creates, not the number of humans using a screen.

Acquire to extend your platform end-to-end so customers cannot go around you. Veeva is a great example of this wherein they have continued to deepen their moat by embedding more and more (eg. clinical trials data and workflows ) into the CRM

And double down on data uniqueness and variety — especially non-digital data like services context, IoT signals, and regulatory intelligence, which AI cannot easily scrape or replicate. ServiceNow’s recent acquisition of Armis is an explicit attempt to augment their workflow & software context with real-time signal data across every connected cyber-asset (including IoT, medical devices etc).

From the bottom-right (workflow orchestration) — move up. You have switching cost. You need data. Three levers:

Launch industry benchmarks using whatever data flows through your workflows, and fine-tune LLMs on that data so it becomes a proprietary asset.

Extend into hardware, IoT, or services data to build a moat that is not just digital.

And shift your business model to outcome-based engagement with multi-modal interaction, not just a SaaS dashboard. Intercom is a strong case study here — they moved from a simple chat widget to an AI-first customer service platform. Fin, their AI agent, went from zero to $100M+ in pure outcome-linked ARR (growing at 350% YoY) by actually resolving customer issues autonomously, not just routing tickets. The real masterclass here involved the Intercom’s founder taking the courageous decision to consciously cannibalize his own core business to reinvent as an AI-first company (while burning the boats to go back from this transition!)

From the bottom-left (basic wrappers) — the hardest conversation. I am not going to pretend this is easy. Most companies in this quadrant will not survive the transition. The honest question a founder has to ask is: can I get to the top-right faster than AI commoditizes what I have today? If the answer is yes, the moves are to fundamentally reimagine the product — not add AI features but rebuild from the ground up. If the answer is no, the most value-creating decision might be to merge with a company that has what you lack, or to sell while you still have customers and workflow to offer. That is not failure. That is smart capital allocation.

What we are seeing in our portfolio

These are not theoretical moves. At Avataar, we have been working with portfolio companies on exactly these transitions. Here are a few examples.

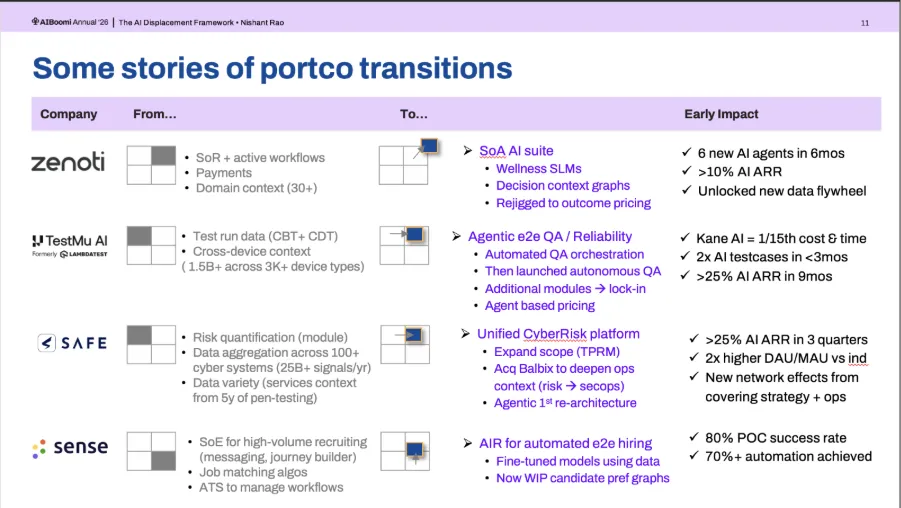

Zenoti started as a System of Record for the wellness industry — scheduling, operations, payments — with domain context across 30+ wellness sub-verticals. Salon is different from medical spa, and they're both very different from fitness. That domain depth was the foundation. They have since built a full AI suite: wellness-specific SLMs, decision context graphs that understand what matters for each sub-vertical, and outcome-based pricing tied to business results, not just seats. Six new AI agents shipped in six months. AI ARR now exceeds 10% of total revenue, and a new data flywheel is compounding as every agent interaction generates signal that makes the next one smarter.

TestMu (fka LambdaTest) had something most companies underestimate: massive test-run data. 1.5 billion+ data points across 3,000+ device types from cloud-based and cross-device testing. They moved first to orchestration — HyperExecute, which parallelized and optimized test execution across infrastructure. That gave them operational context. Then they launched Kane AI with agent-based pricing, automating end-to-end QA autonomously. Kane AI operates at 1/15th the cost and time of traditional testing. They doubled AI test cases in under three months and crossed 25% AI ARR in nine months.

Safe Security began as a risk quantification module — one view of cyber risk across the enterprise. They were aggregating data across 100+ cyber systems & processing 25 billion+ signals per year creating a strong data moat. However, it took an active focus to leverage the 5+ years of pen-testing services context (from an earlier iteration of the company) in order to translate that data + operational context into modern Agentic AI solutions being used for third-party risk management. And we then acquired Balbix to deepen that operational layer — moving from quantifying risk to actually managing it. The unified CyberRisk platform now covers both strategy and security operations. AI ARR exceeded 25% in three quarters, with 2x higher daily active users versus the industry average and new network effects from bridging two sides of the security organization that used to operate in silos.

Sense operates as a System of Engagement for high-volume recruiting — messaging, journey building, job matching algorithms, ATS workflow management. They moved to AI-first architecture with fine-tuned models trained on their proprietary data to create the industry’s first AI Recruiter (AIR) solution. And are now building candidate preference graphs that capture not just what jobs exist but what candidates actually value — pay, proximity, flexibility, growth. Their automated end-to-end hiring product, AIR, hit an 80% POC success rate and 70%+ automation. In this transition, we also discovered something counterintuitive: some enterprise customers deliberately want to dial back autonomy for consent and compliance reasons. The technology can go further than the market is ready to accept. But it’s a constraint worth understanding early.

Each of these companies had real data, real domain expertise, and real customer trust before they started their AI transition. The transition did not threaten them — it gave them a new growth vector. But only because they chose to move, not wait!

The conversation I want you to have

I presented this framework at AI Boomi as the start of a conversation, not a final verdict. It is a tool for self-diagnosis and honest reflection.

Where you sit today matters less than whether you are actively working to move. The founders who will look back on 2026 as the year everything changed are the ones having three conversations with their teams right now: what quadrant are we in, what are the early warning signs showing up in our data, and what do we need to do in the next twelve months to shift. And if this framework is useful, I would genuinely like to hear where you landed — and what you are doing about it.

Indian technology and product is at crucial cross-roads and most global LPs (investors) believe that AI automatically means US-built. They regard the past waves of Services & SaaS as passe mostly due to our country’s inherent cost & labour advantages (which are no longer relevant in an AI-first world). Yet I believe that is only part of the story – it's the unique combination of entrepreneurial spirit, increasing product sensibility & frugal innovation mindset that makes Indian founders and companies worth taking note of.

And while it is true that the US has led the consumer AI wave (GPT, vibe coding etc), In my honest opinion the Enterprise AI wave is only just beginning. In fact, as per an MIT study, barely 5% of AI experiments / tools are shipping to production given Enterprise’s concerns around security, predictable costs, and quality. This is where India has the opportunity to shine. We must leverage our past context (from earlier ITES to SaaS waves) on what it takes to truly be production-ready & fully compliant.

The great news is that every founder (world over) finally has access to the latest AI tech at the same time as US (something which took 5-7yrs even in the cloud era) so there’s never been a better time for us to build!

I hope to get your support to help prove out my hypotheses. And given our #OperatingVC model, if any of us at Avataar Ventures can be of help, we are just one phone call or email away so please don’t hesitate to reach out.

.webp)

.webp)

.webp)

.webp)

_page-0001%20(1).webp)

.webp)