Why We Backed Ethereal Machines: Redefining Precision Manufacturing From Machine to Factory to Software

The hardest parts on earth, the ones inside jet engines, chip-making tools, and surgical robots, are no longer limited by what they cost to make. The binding constraint has moved from cost to capacity. What that means is there are not enough machines, qualified factories, and skilled hands to make these parts as fast as the world now needs them. And that capacity cannot be ordered off a shelf.

It has to be built.

The next defining manufacturers will own how the hardest things get made. Owning the "how" means owning the whole stack: the machine that cuts the part, the factory that qualifies it, and the software that lets the factory learn from every part it runs.

Put those three under one roof and you stop buying precision capacity. You start creating it.

We went looking for the company building exactly that and we found Ethereal Machines.

The world designs hard parts faster than it can manufacture them

For decades, progress in frontier industries was limited by what engineers could design. Could they build a surgical robot with finer control, a satellite light enough to launch cheaply, a turbine blade that survives higher stress? Design software, simulation, and cheap computing have made that work faster than ever. But the physical world has not kept pace.

Products are evolving toward fewer parts that are harder to make

The Boeing 747 had 6 million parts. The Boeing 787 has 2.3 million. The newer aircraft is not simpler. It is harder. Half its airframe is carbon-fibre composite, the engines run hotter, and the tolerances allow almost no margin for error. As the part count fell, the difficulty concentrated into the parts that remained.

The manufacturing system that made the Boeing 747 generation cannot make the Boeing 787 generation.

A different discipline has to emerge.

The same shift is underway across other industries. Aerospace components must survive heat, pressure, vibration, and fatigue cycles measured in decades. Similarly, semiconductor tools hold position to the nanometre. Premium electronics have turned a phone's enclosure into a micron-tolerance precision system with dozens of finishing steps. Surgical robots, satellites, EV drivetrains, wind turbines, and drug-delivery devices are all becoming smaller, more integrated, and more regulated while becoming less forgiving of failure.

What they share is a punishing new standard: tighter tolerances, and almost no room for error.

Case in point: How a speck of dust took down a $7bn supply chain

In 2023, a contamination smaller than a grain of sand entered the metal powder used to make high-pressure turbine discs at Pratt & Whitney. These parts spin above 10,000 RPM at gas-path temperatures that would melt steel. The flaw seeded structural weak spots in more than 600 commercial jet engines. Airlines grounded planes for up to 300 days each, and the industry absorbed $7 billion in costs. In India, one airline caught in this was Go First. It had grounded a big chunk of its fleet because of these engine problems, and it collapsed into bankruptcy in 2023.

This is a classic example of where conventional manufacturing breaks. Tolerances move from millimetres to microns, and in the most demanding work into the single digits, finer than a single strand of human hair. Defect rates fall to a few parts per million, fewer than three failures in a million, and at that level the cost of getting it wrong is no longer measured in scrap.

Precision engineering is the answer, but the capability is hard to build

Avoiding that kind of failure is the entire job of precision engineering: making parts that perform exactly as designed, repeatedly, under stress, for years. The knowledge of how to do it sits in a handful of factories, and the machines, though they matter, are not the only moat.

That knowledge of how titanium behaves under stress, the few microns a coating can shift a finished dimension, the early signs of process drift before it becomes a defect is specific and hard-won.

It lives inside the operators, engineers, and quality systems of a single factory floor, and it takes years to build. It cannot be hired in or carried away when a machine is sold.

That also means that once a supplier is qualified, the moat deepens. Switching vendors would mean new audits, new first-article inspections, new failure modes, and new production risk, so the longer a relationship holds, the harder it becomes to dislodge.

Precision engineering decides what the world can ship

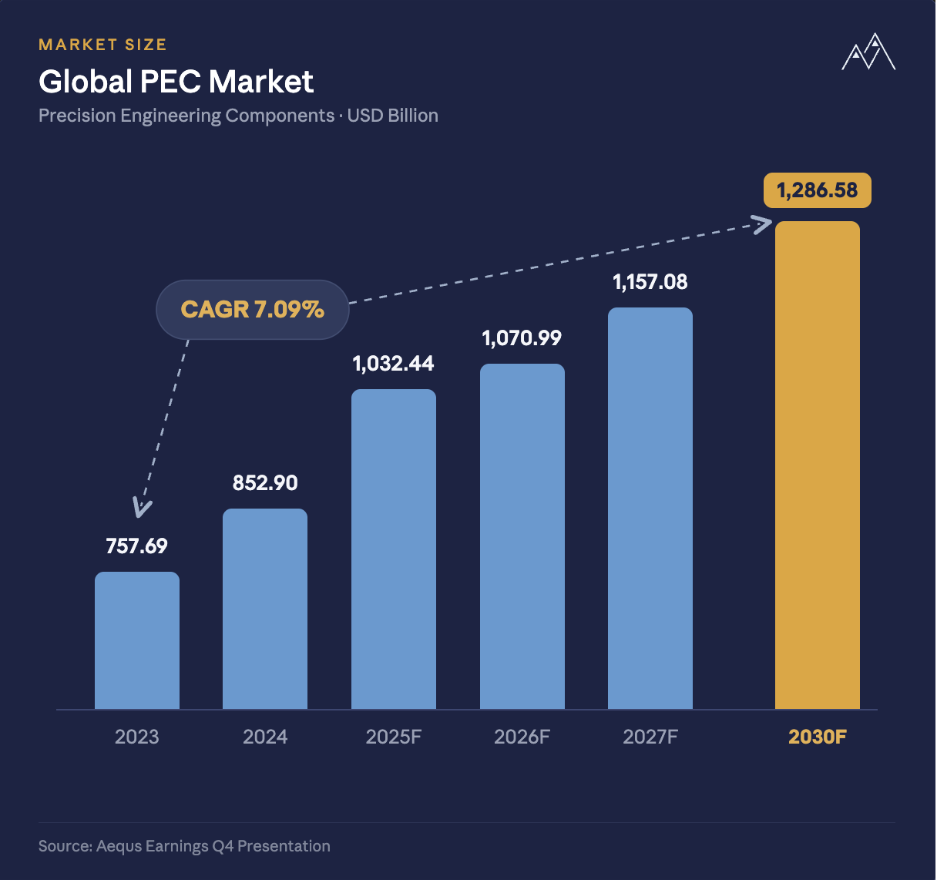

The money is moving toward difficulty. The global precision engineering market is already $1 trillion, but the value is concentrating in its hardest corners like aerospace, defense, semiconductors, energy, and medical devices, which are growing 10 to 20% a year (vs. 7% overall industry). The harder the part, the faster its market is growing.

No frontier industry can move faster than its hardest components can be designed, qualified, and manufactured. Precision engineering is the bottleneck between what the world can design and what it can ship, and whoever masters it sets the pace of the next industrial era.

The old precision supply chain is breaking

The bottleneck is no longer theoretical. The supply of the world's hardest parts was built by a handful of countries over fifty years, and it is now buckling under demand it was never designed to carry.

Demand for precision is exploding everywhere at once

In aerospace, the combined Airbus and Boeing backlog tops 14,000 aircraft, 11 to 12 years of production worth $972 billion.

In semiconductors, TSMC is spending around $60 billion in 2026 and still cannot make enough advanced chips, because the machines that build them are themselves scarce: a single ASML EUV scanner takes 18 months to assemble from a handful of suppliers in Germany, the Netherlands, and Japan.

In energy, AI data centers now draw more power than the US grid can supply, and the two viable backstops, gas turbines and fuel cells, are both precision-made and capacity-constrained, with the gas-turbine queue running into the 2030s.

In pharma, GLP-1 supply is rationed less by the drug than by the precision-moulded pens that inject it, which is why Eli Lilly has committed $50 billion to new US manufacturing through 2030.

The pattern holds in every case: the largest companies in the world cannot deliver what they have already sold.

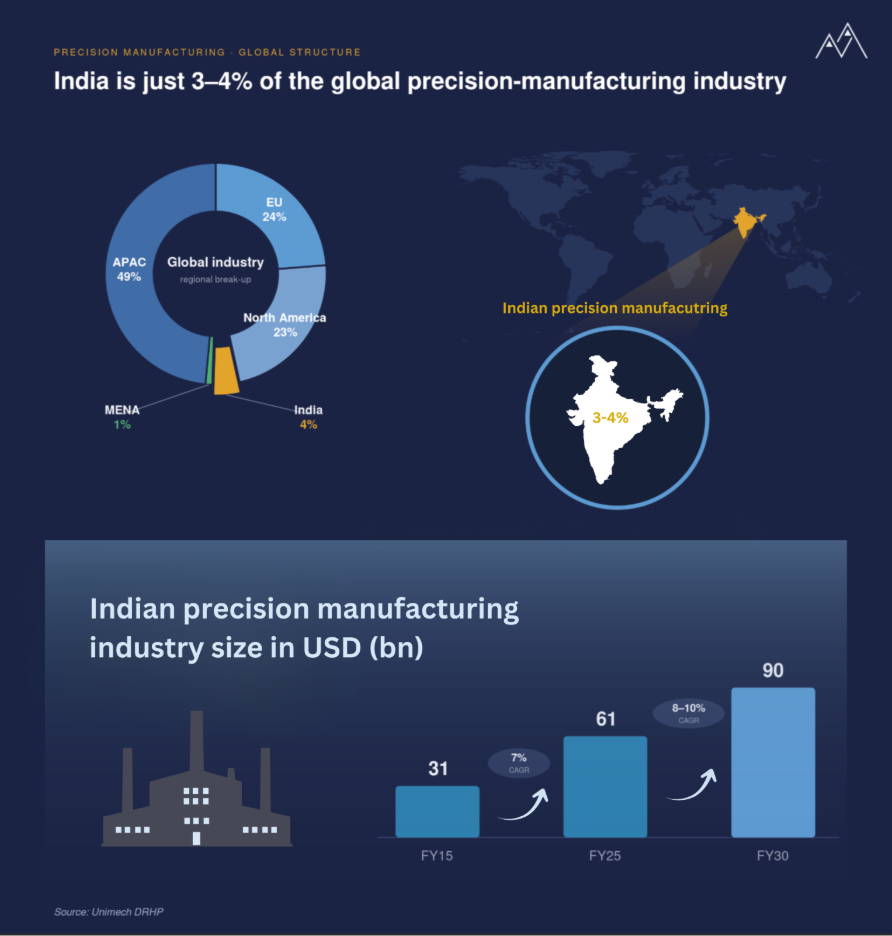

This demand falls on a tightly concentrated supply base: APAC holds 49%, the EU 24%, North America 23%, and India about 4% of the global precision engineering market. The high-end work, for aerospace, semiconductors, defense, and medical devices, sits with Germany, Switzerland, Japan, and the United States, while China dominates the large-volume layer that supplies consumer electronics, automotive components, and industrial machining.

This arrangement held for fifty years. It is breaking now.

The West can't expand fast enough to meet it

Expanding the Western base would once have been the obvious answer. Three things now prevent it.

- Labour: skilled-machinist attrition has nearly doubled, from 4.3% in 2017 to 7.1% in 2023, and about 30% of the workforce is near retirement with few entering the trade.

- Cost: Western machinist rates run €35 to €70 an hour against €8 to €15 in India, and EU industrial electricity costs two to three times what the US or India pays.

- Capacity: suppliers now turn away RFQs every week for lack of slots, COVID erased roughly 20% of the supplier base, and much of what survived runs on equipment built before modern automation. The West cannot expand fast enough to carry the next industrial cycle.

China is no longer the default answer

China built one of the most formidable manufacturing ecosystems in history, and it still holds a real cost advantage. What has changed is less about China than about how customers now weigh risk. Procurement teams in strategic industries increasingly price in geopolitical concentration, export controls, and IP exposure alongside cost and quality, and on that scorecard a single-country dependence on China has become harder to justify.

Other geographies absorb only part of the shift

The alternatives are real but partial. Mexico has proximity to the US but is already capacity-constrained in its best industrial corridors. Vietnam is a strong electronics hub but thin in aerospace and high-reliability precision. Morocco has built automotive and aerospace adjacencies, though not yet at India's engineering depth. Eastern Europe has talent and proximity but increasingly Western European costs.

No single country replaces China; each absorbs the slice it can.

New capacity is hard to build

Even if a new precision hub wanted to emerge from scratch, it would hit a second, less visible constraint. The precision capex itself is scarce.

Industrial 5-axis CNC manufacturing is an oligopoly, fewer than ten firms, mostly in Germany and Japan, running 6-to-12-month backlogs, and the last new entrant to the category was Haas Automation in 1983.

As every advanced industry ramps up at once, every shop on earth is lining up for the same machines. But the scarcity runs deeper than hardware. Advanced controllers, tooling, metrology, qualified operators, and special-process certifications all scale slowly, and for aerospace and defense the controllers themselves often need export licenses.

Additive manufacturing is scaling alongside this, but it compounds the constraint rather than relieving it. For example: 3D-printed parts still need five-axis finishing on their critical surfaces, so they flow into the precision-machining queue, not around it.

The world cannot build new precision capacity fast enough to match demand. That is the real constraint. The bottleneck is capacity itself, and capacity is slow to build. Every machine has a year-long queue, every new supplier takes years to qualify, every process must be learned by hand.

So the advantage in the next decade goes to whoever can create precision capacity, not just buy it.

A new precision map is being drawn

The supply chain that took fifty years to build cannot answer the demand of the next decade, and buyers know it. They are not waiting for a perfect solution: commitments are being signed, sourcing redirected, and new hubsare being qualified.

Clusters are also being tested across India, Mexico, Morocco, Vietnam, Eastern Europe, and Southeast Asia, and each will absorb part of the shift. None will win on cost alone.

India is where the next precision hub gets built

India is one of the few countries with what it takes to win on more than cost. It has the engineering depth, the operating discipline, and the historical pattern of climbing the capability ladder over decades. And it has the timing: a once-in-a-generation realignment in global supply chains has opened a door that rarely opens.

India already has what the work demands

The raw materials are in place.

- Engineering: India graduates more than 1.5 million engineers a year, over ten times the United States, with real operating depth across manufacturing, aerospace, electronics, software, and R&D.

- Cost: a CNC machinist who earns around $60,000 a year in the US earns closer to $3,000 in India, in an industry where labour can be nearly half the cost of a part.

- Policy: PLI schemes, aerospace and defense corridors, semiconductor incentives, and FDI liberalization have steadily tilted the field toward domestic manufacturing.

The biggest shift, however, is trust.

India has climbed this capability ladder before

Over the last three decades, India has run the same playbook in one industry after another: enter at the low-complexity end, build operating discipline and customer trust over years, then climb toward higher-value work and system-level ownership. It did this in autos, pharma, electronics, and most visibly in software, moving from low-margin IT services to globally-licensed SaaS.

Precision manufacturing is the next climb.

The first large-scale example was automotive. What began in the 1990s as low-value castings and forgings is now one of the world's largest auto-component ecosystems, more than $20 billion in annual exports, with Bharat Forge, Motherson, and Sona BLW supplying global OEMs. It climbed from labour arbitrage to process capability to global trust over three decades.

That same capability is now moving into harder sectors, aerospace, defence, semiconductors, and medical systems. India's aerospace precision-engineering exports have grown from roughly $500 million a decade ago to more than $2 billion today, at a high-teens CAGR, and the mix is shifting from basic machining into qualified components, assemblies, tooling, aero-engine parts, and special processes, work where qualification takes years and customers rarely switch.

A new generation of companies is already across the threshold.

Aequs (~$1B market cap) started in 2007 with aerospace machining and built India's most vertically integrated aerospace platform, qualified across Airbus, Boeing, Collins, and Safran, now extending into precision components for Apple's India supply chain.

Azad Engineering (~$1.2B market cap) started in 2008 as a small energy-components machining shop and is now a Tier I supplier to GE Vernova, Mitsubishi Power, Siemens Energy, Baker Hughes, GE Aerospace, Rolls-Royce, Honeywell, Safran, and Boeing. In 2026, it won a DRDO contract to manufacture India’s first indigenous jet engine, marking its shift from component supplier to systems integrator.

Unimech Aerospace (~$700M market cap) started in tooling and within a decade scaled into a high-margin platform supplying complex tooling, aero-engine components, and ground-support systems to global OEMs.

Global OEMs are voting with their sourcing

That growing trust now shows up in the public sourcing commitments of the world's largest industrial companies. In aerospace, Boeing plans to raise India sourcing fivefold to $1.25 billion by 2030, Airbus to double it to $1.5 billion by the end of the decade, Safran to more than €3 billion of annual India revenue by 2030, Collins to triple its India sourcing, and Rolls-Royce to double its own.

The pull extends well beyond aerospace. Apple's India manufacturing base has grown fast, but the more important question is what comes after assembly: the next layer of value sits in enclosures, connectors, cables, PCBs, power components, and precision metal parts, and as assembly scales, that component ecosystem has every reason to deepen.

India’ low penetration (<3-4%) of the Global Precision Engineering market combined with improving manufacturing capabilities and supply-chain diversification, positions India for multi-year share gains

The qualification window is closing

This imbalance will not stay open forever. Backlogs will normalise and new suppliers will embed inside long-duration programs. That is what makes this qualification cycle so important: companies that earn trust now are likely to stay embedded in global manufacturing ecosystems for decades.

The winners will be capability platforms, not job shops

India's lack of an industrial inheritance is, in this sense, its advantage. Many of the precision engineering companies being built there today are software-native and automation-first, designed around modern global supply chains rather than retrofitted from legacy workflows. They are building precision capability from scratch, not patching up old factories.

Solving such structural bottlenecks requires more than just a cheaper machine shop. The winners will not be the suppliers who sell machine hours most cheaply.

The winners will be the ones who can build precision capacity itself, by owning the whole stack: the machine, the factory, the software, the IP. Ethereal Machines is what that looks like in practice.

Ethereal Machines is our bet on Indian precision manufacturing

Aequs, Azad, and Unimech have proved India can build precision at scale. They imported world-class machines, qualified with global customers, and earned OEM trust over decades. A different kind of company is now being built in India, and the story of Ethereal Machines starts with the machine itself.

The machine changes the cost of creating capacity

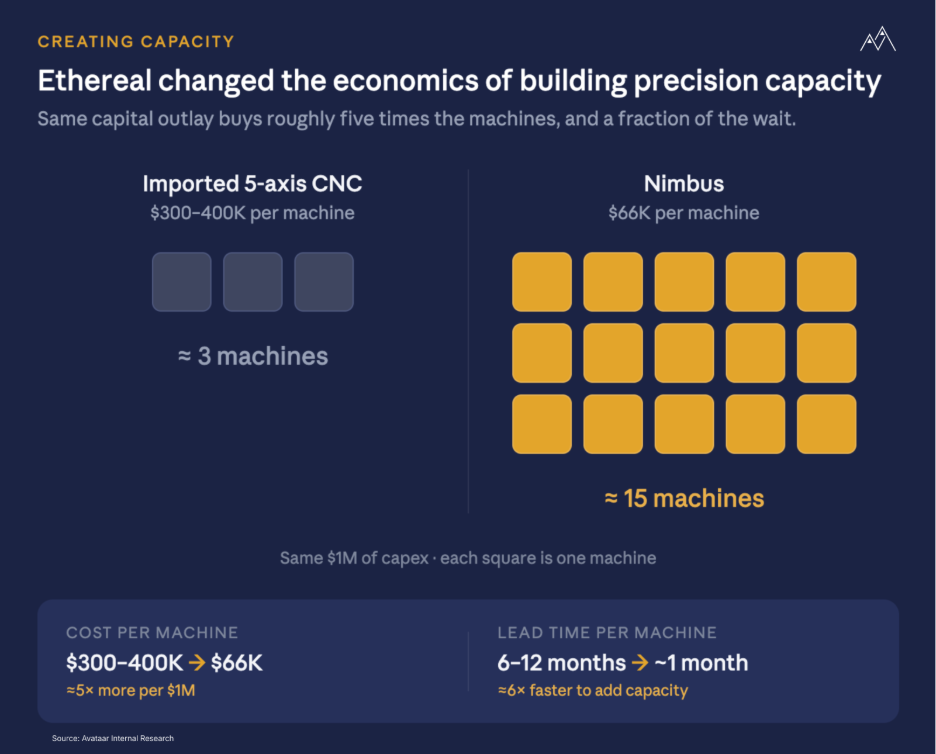

Most precision shops buy theirs from Germany or Japan, where a five-axis CNC runs $300,000 to $400,000. To pay that back, a shop must keep it busy with at least one high-margin vertical like aerospace, defense, or medical, because spreading that capex across markets is not affordable.

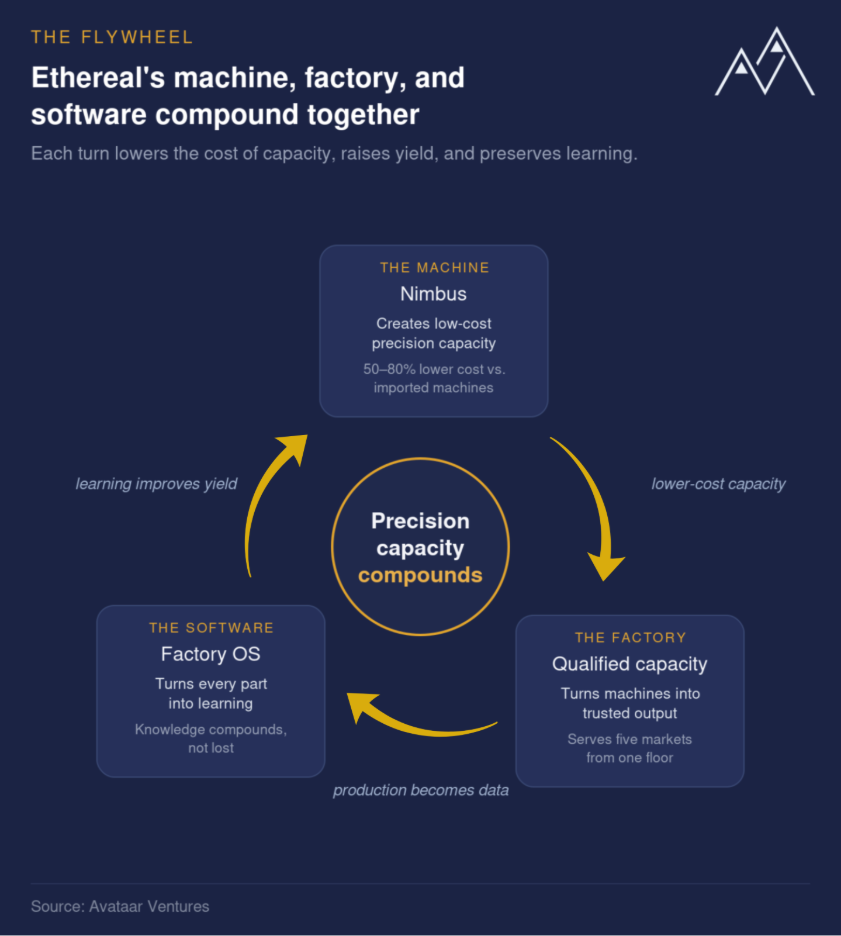

Ethereal did not buy the machine. It built one.

In 2014, Kaushik Mudda and Navin Jain were engineering students at RV College in Bangalore, and the five-axis CNC they needed was beyond their reach, so they built it. Thirteen prototypes later, they had a production-grade machine. They called it Nimbus.

Nimbus cost about $66,000 to build, roughly a fifth of the ~$300,000 a global machine-tool builder like DMG Mori charges, and it could be ready in about a month against the six to twelve months it takes to import one.

That reset the company's starting point. The fleet grew nearly sixfold in the first year, but there was a deeper shift: Ethereal had changed the cost of creating precision capacity itself.

Then came the more important decision. Ethereal did not sell Nimbus; it kept the machines and built a factory around them and that is the core of our bet.

The factory turns capacity into qualified output

In precision manufacturing, supply is the constraint.

Customers do not need cheaper parts; they need qualified capacity that can scale without breaking quality. Ethereal owns the machine that creates the capacity and the factory that turns it into qualified output, and because its cost of adding capacity is lower, it can serve five markets at once without forcing each to carry the full burden of imported-machine economics: aerospace and defense, healthcare, semiconductor capital equipment, consumer electronics, and energy.

The tolerance was learned on semiconductor tooling; the material was learned in aerospace; a specific inspection method was learned in medical devices and each of these learning instances improved the next job the factory runs. But how does this multi-faceted training work in a manufacturing unit?

The software turns the factory into a learning system

The software is what makes that learning compound.

Every Nimbus on the floor runs on Factory OS, built by the same team that built the machine, so every part, rejection, inspection, and adjustment becomes part of the factory's memory. In most factories that memory is fragile, held in the heads of the machinist who knows how a material behaves, the process engineer who can sense a tolerance about to drift, the quality lead who spots a failing batch, and it leaves when they do. Ethereal makes it systematic, so the knowledge stays with the factory rather than the person.

Why we backed Ethereal

Scaling a precision shop is hard for largely three reasons: machines are expensive, process knowledge takes years to build, and customer trust is slow to earn. By owning the full stack, Ethereal attacks all three at once, and its qualification record compounds into trust.

There is one last factor, and it is the most important: the founders.

Building any company out of India is hard. Building technology no one in the world had built since 1983, refining it prototype after prototype, in a factory shed in Bangalore on almost no outside money, is a different kind of hard.

It takes a rare mix of conviction and endurance to carry a company through the years this one has survived. Very few founders would make it through, let alone emerge stronger. Kaushik and Navin are that rare breed, and this is what they have built.

We began with our conviction: the defining manufacturers of the next decade will own how the hardest things get made. Ethereal is that company, the machine, the factory, and the software under one roof, creating the precision capacity the world cannot simply buy, and doing it from India against odds that would have stopped almost anyone else.

We are convinced it will be one of the defining industrial companies of its generation. That is why we backed it.

Sources & References

Section 1: The world can design hard parts faster than it can manufacture them

Boeing 747 part count (~6 million): Aviation Week & Space Technology archives; Boeing Commercial Airplanes historical specifications.

Boeing 787 part count (~2.3 million) and 50% composite airframe: Boeing 787 Dreamliner technical specifications and Boeing Annual Report.

Tolerance and Six Sigma defect benchmarks: ISO 9001:2015 manufacturing standards; SAE International AS9100 (aerospace) standards documentation.

Pratt & Whitney PW1100G powder metallurgy contamination (2023): RTX Corporation 2024 10-K filing; FAA Airworthiness Directive 2023-22-01; Bloomberg, Wall Street Journal, Reuters coverage 2023-2024.

Go First bankruptcy: NCLT filings (May 2023); Indian business press coverage.

Global precision-manufacturing market ($1.5-1.8 trillion, ~7% CAGR; strategic non-auto segments at 10-20%): Avendus Spark Research, Precision Manufacturing Thematic Initiating Coverage, January 2026; Crisil MI&A; Frost & Sullivan.

Section 2: The old precision supply chain is breaking

Airbus and Boeing aircraft backlog (~14,000 aircraft, $972 billion): Airbus and Boeing Annual Reports; Stifel Aerospace & Defense Market Update 2024.

TSMC 2026 capex (~$60 billion): TSMC Q3 2025 earnings call; capex guidance.

ASML EUV scanner build time (~18 months): ASML Annual Report 2025; SEMI Industry Reports.

Bloom Energy US fuel-cell capacity doubling: Bloom Energy investor communications 2025.

Eli Lilly $50 billion US manufacturing commitment through 2030: Eli Lilly press releases 2024-2025.

Global manufacturing share (China ~30%, US ~17%, Japan ~6%, Germany ~5%, India ~3%): World Bank manufacturing value-added data; UN Industrial Development Organization (UNIDO).

Regional precision-manufacturing share (APAC 49%, EU 24%, North America 23%, India ~4%): Crisil MI&A; Frost & Sullivan; Avendus Spark Research.

Western machinist attrition data (4.3% in 2017 to 7.1% in 2023, US average 3.8%; ~30% of workforce nearing retirement): US Bureau of Labor Statistics; Eurostat manufacturing labour data; Reshoring Institute.

Western machinist hour rates (€35-70) and Indian rates (€8-15); EU industrial electricity cost premium: Reshoring Institute; Eurostat industrial electricity prices.

COVID-19 erosion of Western supplier base (~20%): Reshoring Institute; industry surveys.

Chinese manufacturing wage growth (10x since 2000, $0.60 to over $6 per hour): China National Bureau of Statistics; Reshoring Institute.

Yanjun Xu / GE Aviation IP-theft case: US Department of Justice press releases (October 2018 indictment, November 2021 conviction, November 2022 sentencing); FBI public statements.

5-axis CNC oligopoly (fewer than 10 global firms, 6-12 month backlogs, 60%+ gross margins): Modern Machine Shop industry analysis; DMG Mori, Mazak, and Hermle annual reports; CNCCookbook research.

Section 3: India is where the next precision hub gets built

Indian engineer graduates (1.5 million annually) vs US (~130,000): All India Council for Technical Education (AICTE); NASSCOM Strategic Reviews; National Center for Education Statistics (US).

CNC machinist salary comparison (US ~$60,000 vs India ~$3,000): US Bureau of Labor Statistics; PayScale India.

Indian PLI schemes, FDI liberalisation, aerospace/defence corridors, semiconductor and medical-device incentives: Department for Promotion of Industry and Internal Trade (DPIIT); Press Information Bureau (PIB); Ministry of Electronics and IT (MeitY).

Indian electronics manufacturing (0.2% of US smartphone imports in 2018; ~14% of global iPhone production in 2024, ~32% target by 2025; Apple 14 to ~40 India suppliers): India Cellular and Electronics Association (ICEA); Apple supplier disclosures; multiple India business press.

Indian pharmaceuticals (40% of US generic drug supply; ~1 in 4 vaccines globally; Serum Institute ~1.5 billion doses/year): IQVIA Institute; WHO procurement data; Indian Pharmaceutical Alliance; Serum Institute communications.

Indian software industry ($254 billion FY24; Zoho $1B+ ARR; Freshworks NASDAQ-listed; AI foundation model players Krutrim and Sarvam): NASSCOM Strategic Review 2024; company disclosures.

Indian Engineering R&D services market (~$45 billion, ~1,800 GCCs serving ~50% of Fortune 500; chip design centres for Intel, Nvidia, Qualcomm, AMD): NASSCOM ER&D Reports; ANSR India GCC Survey.

India space sector (Chandrayaan-3 lunar landing 2023; ISRO budget under $1.5 billion until 2020; Skyroot, Agnikul, Pixxel): ISRO Annual Reports; IN-SPACe data; company disclosures.

India auto-component exports ($20+ billion; world's second-largest forgings producer): Auto Component Manufacturers Association of India (ACMA); Society of Indian Automobile Manufacturers (SIAM).

India aerospace precision-engineering exports ($500M a decade ago to $2B+ today, high-teens CAGR): SIDM (Society of Indian Defence Manufacturers); Ministry of Civil Aviation.

Aequs, Azad Engineering, Unimech Aerospace data (revenue, market cap, customer base, business mix): Company DRHPs; ICICI Securities, Avendus Spark, and Goldman Sachs equity research coverage; company annual reports.

OEM India sourcing commitments (Boeing $1.25B by 2030, Airbus $1.5B by end of decade, Safran €3B by 2030, Collins Aerospace tripling, Rolls-Royce doubling): OEM India-day disclosures and supplier-day press releases.

Section 4: Ethereal Machines is our bet on Indian precision manufacturing

Ethereal Machines founding (2014, RV College Bangalore, Kaushik Mudda and Navin Jain): Ethereal Machines investor materials; company website; Blume Ventures portfolio commentary, May 2025.

Five-axis CNC pricing ($300,000-$400,000 imported, ~$66,000 Nimbus build cost): Ethereal Machines investor presentation, June 2025; supplier quotations.

Ethereal Machines fleet, utilisation, ROCE, gross margins, customer-base data: Ethereal Machines investor materials; Avataar Ventures investment committee diligence.

Ethereal customer base including HAL, BEL, Collins Aerospace: Ethereal Machines company disclosures.

FANUC and Siemens controller market share (50-65% combined): Modern Machine Shop industry analysis; CNC industry research.

BAFA and METI export-control regimes: German Federal Office for Economic Affairs and Export Control (BAFA); Japanese Ministry of Economy, Trade and Industry (METI) export control regulations.

.webp)

.webp)

.webp)

.webp)

_page-0001%20(1).webp)

.webp)